By Bakary Traoré, Economist, OECD Development Centre, and Elisa Saint-Martin, Junior policy Analyst, OECD Development Centre

A review of on-going industrial strategies (Africa’s Development Dynamics 2019 report) shows that most African countries have the ambition to expand processing activities in sub-sectors such as agro-industries, fertilisers, metals and construction materials. To achieve this, it is urgent to improve the quality of energy supply across the continent. Regional co-operation for energy among Africa’s cross-border intermediary cities can be a game changer.

A review of on-going industrial strategies (Africa’s Development Dynamics 2019 report) shows that most African countries have the ambition to expand processing activities in sub-sectors such as agro-industries, fertilisers, metals and construction materials. To achieve this, it is urgent to improve the quality of energy supply across the continent. Regional co-operation for energy among Africa’s cross-border intermediary cities can be a game changer.

First, let’s take a look at the main challenges

Today, industrial processing activities and transport services account for no more than 35% of total energy consumption in Africa (see Figure 1, based on the OECD/IEA 2019 database). Africa’s electrical networks are struggling to cope with current needs: on average, firms in sub-Saharan Africa face 8.5 electricity outages a month (World Bank, Enterprise surveys, 2019), and 40.5% of them consider insufficient access to energy to be a major constraint to their growth and competitiveness.

Between 2018 and 2040, Africa’s energy demand is expected to grow twice as fast as the global average (IEA, 2019). In Sub-Saharan Africa (excluding South Africa), demand for energy will quadruple, increasing at an average rate of 6.5% annually [1]. Demand from industry and services sectors is likely to increase at a rate of 6% annually over the same period. Responding to increasing demand will require more investment, not just in power generation, but also in transmission and distribution infrastructure. The level of investment required to achieve universal access to energy in Sub-Saharan Africa is estimated at USD 27 billion per year (2018-2030); at least twice the current levels of energy financing (Corfee-Morlot, 2019).

Public-led investment programmes alone will not be enough to fulfil the need for more energy. Yet, in 34 countries out of 43 in Sub-Saharan Africa, current regulatory frameworks for energy supply do not allow private sector participation in transmission and distribution activities (IEA, 2019). Mobilising funds for the energy sector remains difficult. Despite significant efforts by power pool initiatives [2] to set up mechanisms and regulatory bodies for power trading across Africa’s regions [3], governments have made timid progress in financing interconnection infrastructure. In many cases, countries’ motivation to incur energy interconnection costs is limited, as they tend to see these investments as an extra cost that does not always translate into electricity generation (ECDPM, 2019).

In this context, intermediary cities can be a game changer in finding cost-effective solutions for energy

Small and medium-size cities are likely to account for a large share of the increase in Africa’s demand for energy. With an urban population set to double over the next 25 years, Africa is going through a rapid urban transition, mainly taking place in intermediate cities and towns with under 500,000 residents. They accounted for 67% of urban growth between 2000 and 2018 (AfDB/OECD/UNDP, 2016). In this context of rapid urbanisation, promoting productive activities in intermediary cities will play a crucial role in connecting Africa’s rural-urban supply chains and helping local small and medium enterprises meet regional demand. Countries stand to benefit from expanding energy supply to productive activities, such as food processing, agricultural input supply services, logistics or warehousing facilities. In Côte d’Ivoire, Coulibaly et al. (2014) found that when the location quotient, or concentration, of firms increases by 10% in intermediary cities like Daloa (in the centre-west sub-region) or in Odienne (in the northwest sub-region), firms operating there increase their sales by 15%, and 17% respectively. In contrast, the effect is negative for Abidjan: a 1% increase in the location quotient in Abidjan is associated with a decrease in sales by 10%, indicating that congestion costs prevail in this city of 4 million inhabitants.

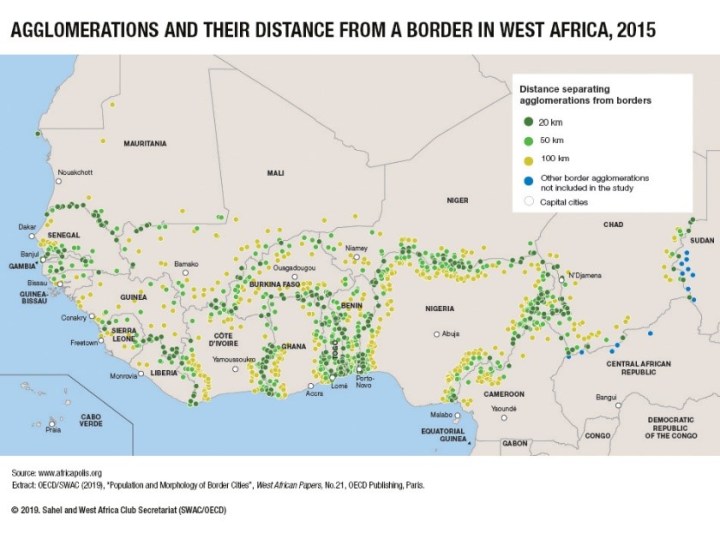

The short distances between border cities is conducive to regional co-operation and many of Africa’s intermediary cities are located within 50 km of countries’ borders (see Map 1 for example). Furthermore, population in West African border cities has been growing even faster than in other cities (OECD/SWAC, 2019). Neighbouring countries are starting to take advantage of this geographical proximity between cities by establishing cross-border special economic zones. For instance in 2018, Burkina Faso, Côte d’Ivoire and Mali launched SKBO, West Africa’s first cross-border special economic zone. It aims to encourage agro-industrial and mining companies to set up in the area spanning between the cities of Sikasso, Korhogo and Bobo Dioulasso (AUC/OECD, Africa’s Development Dynamics 2018). And in March 2019, Ethiopia and Kenya announced their plan to convert the Moyle region into a cross-border free trade zone (UNCTAD, World Investment Report 2019).

Map 1

These cross-border special economic zones are promising and cost-effective solutions for regional co-operation in renewables. Cross-border special economic zones can provide the scale required to accelerate the deployment of renewables in Africa, and therefore narrow the disconnect between their immense potential, and current investment trends. Despite noticeable progress in developing renewable energy in a few African countries between 2010 and 2018 (IEA, 2019, p368), around 93% of Africa’s economically viable hydropower potential remains unexploited (UNEP, 2017). A major shift towards modern energy sources, such as renewables and natural gas, and improved energy efficiency, can help Africa fuel an economy four times larger than today with only 50% more energy by 2040 (IEA, 2019). Gains are also sizeable in terms of energy generation costs in light of the falling costs of renewable technologies (IEA, 2019 Renewables Market report).

Africa needs to energise its productive transformation, especially in job-intensive sectors. The dynamism of intermediary cities brings great opportunity to achieve this, if countries join forces through regional co-operation.

[1] In comparison, energy demand in sub-Saharan Africa increased at an annual average rate of 3% between 2000 and 2010, and then 2.5% annually over 2010-18.

[2] Africa is home to five regional power pools: Eastern Africa Power Pool (EAPP); Central African Power Pool (CAPP); Southern African Power Pool (SAPP); West African Power Pool (WAPP); and Maghreb Electricity Committee (COMELEC).

[3] For example, WAPP has its Regional Electricity Regulatory Authority (ERERA) based in Accra. In East Africa, EAPP has an Independent Regulatory Board (IRB) based in Addis Ababa. In Southern Africa, SAPP has a Regional Electricity Regulatory Association (RERA).